Payment facilitation operations combine payment processing, merchant management, and regulatory compliance to help businesses offer embedded financial services at scale. Developing a payment facilitator solution involves integrating payment gateways, automating merchant onboarding and verification, implementing risk assessment tools, and managing transaction settlements. To maintain profitability and compliance, companies also need robust fraud prevention systems, scalable infrastructure, and continuous adherence to PCI DSS, AML, and KYC requirements.

The sweeping growth of eCommerce over the past decade boggles the mind: according to Grand View Research, the eCommerce sales are projected to constitute $8.1 billion in 2026.

The pace at which eCommerce has been growing has created the need to improve the business processes within it and look for new ways of meeting the ever more sophisticated demands of the ever growing eCommerce audiences. The advent of marketplaces (like, for example, eBay and Amazon) became the true game changer: the possibility for buyers and sellers to easily switch roles multiple times whenever required necessitated introducing a payment-handling scheme that would not require opening a merchant account every time it was required. And this is how the payment facilitator (or PayFac) came into being.

Becoming a PayFac could be a worth-considering venture, so before you start, let’s dwell on the essence of payment facilitation as a business and discover its advantages, while keeping technical and compliance considerations in mind.

What Is Payment Facilitation?

Payment facilitation means an approach based on the aggregation of payments by a party called PayFac (also referred to as a merchant service provider) that provides a payment gateway and collects payments from merchants on behalf of an acquirer. Thus, according to the payment facilitation definition, this approach eliminates the hassle of opening traditional accounts for merchants, enabling faster and more seamless transaction processing. PayFacs allow merchants to accept credit cards, debit cards, as well as some other electronic payments.

Good payment facilitation examples are such well-known providers as Stripe, PayPal, Stax Stripe, and many others. In addition, there are also banking institutions that offer merchant services, like, for example, Chase Bank or Wells Fargo.

Next, we’ll use our vast experience in fintech and eCommerce software development to look at how PayFac works in more detail.

Traditional Acquiring Vs. Payment Facilitation

To better understand the meaning and benefits behind PayFacs, one should look at the several illustrative differences between facilitation of payments and traditional acquiring.

Traditional acquiring kicks off with a merchant signing a contract with an acquirer, or financial institution that then accepts and processes payments on their behalf, acting as an intermediary between the merchant and a credit card network, such as, for example, Mastercard. With payment facilitation, a merchant doesn’t have to go through the lengthy hassle of opening a merchant account (the procedure may take weeks) and dealing with lots of the related paperwork.

In the case of traditional acquiring, a merchant uses an account with their bank to accept payments of all the types they deal with. With payment facilitation, a merchant uses PayFac’s master bank account: they can receive payments quickly and handle all their transactions centrally, which spares them a great deal of daily drudgery.

Lastly, with payment facilitation, merchants don’t have to work with several financial providers separately.

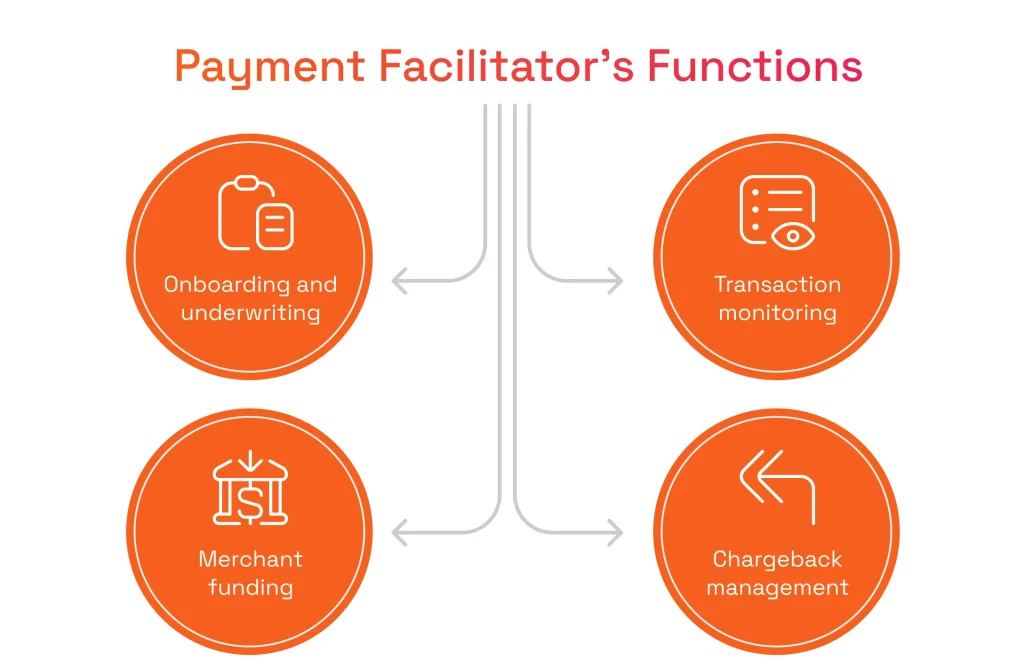

The Functions Payment Facilitators Perform

Onboarding and Underwriting

Just like a merchant bank, a PayFac is obliged to properly onboard a merchant. This means that prior to beginning to receive payments via this PayFac, a merchant must undergo a procedure called underwriting, whereby the merchant is vetted with a view to making sure they are not associated with any negative factors (e.g. corruption, bribery, fraud, or other unethical practices).

Underwriting renders the merchant-PayFac relationship compliant with the applicable regulations. In particular, this includes a KYC procedure with checks against various black lists, like, for example, Mastercard’s Master Alert to Control High-Risk Merchants list. In most instances, PayFacs use specialized KYC software to automate their onboarding and underwriting procedures. This is a major time-saving convenience for merchants being onboarded.

Transaction Monitoring

A payment facilitators’ obligations as to their merchant clients being bona fide are not limited to the underwriting procedure that takes place at the start of their cooperation. They must also regularly monitor their clients transactions, making sure their activities stay compliant with various Government regulations, as well those imposed by the credit card networks, like, first of all, PCI DSS.

Merchant Funding

To provide a better and more comprehensive service, many payment facilitators engage in funding or paying out of funds that are due to their merchants. This frequently allows them to reduce the time required for payouts to take place and creates another tangible benefit for their client merchants, in particular, SMEs.

Chargeback Management

Along with their acquirers, payment facilitators must get involved in investigations whenever customers dispute charges. They are also liable for the amount of a transaction in the event they cannot recover this amount from the corresponding merchant. In the case of Traditional Acquiring, the process is handled by the issuing bank that approaches the credit card company involved.

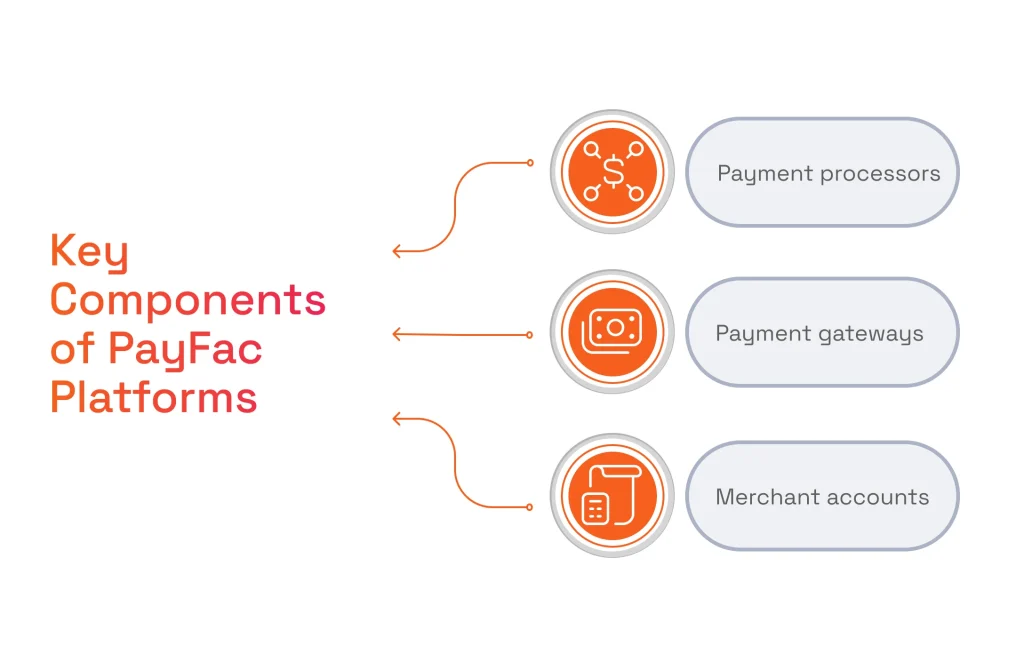

How Do Payment Facilitators Work and Make Money?

Payment facilitators are essentially Fintech businesses that allow merchants to centrally accept payments of different types regardless of the credit card network or payment system the payment originates from. To enable this, they open a master merchant account that can be used to accept payments from multiple merchants.

So, how do these components interact to form a PayFac ecosystem?

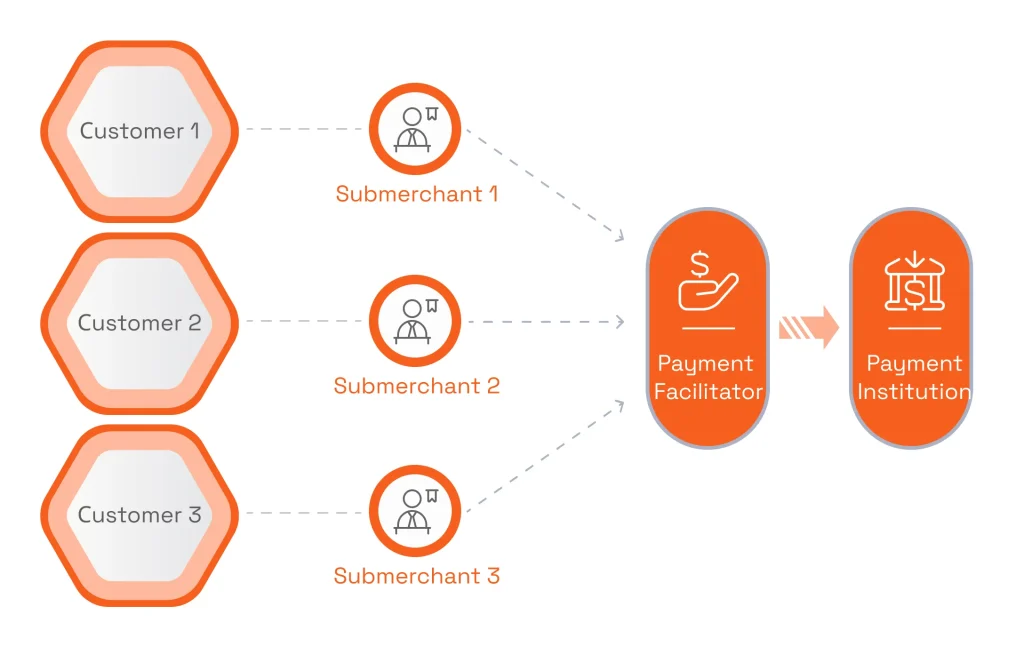

How Payment Facilitation Works as a Process

To gain insight into the mechanics of payment facilitation, let’s examine a specific scenario involving a credit card transaction. The processing of this transaction would loom as follows:

- The process starts with a customer making a payment in favor of a sub-merchant using a credit card. The request to authorize the payment is received by the payment processor the PayFac works with.

- The payment processor validates the transaction and forwards it to the corresponding credit card network for further validation. Upon confirmation, the credit card network sends an authorization back to the payment processor.

- Following this, PayFac’s bank settles the transaction and transfers it for further processing.

How Do PayFacs Make Money

According to the payment facilitator model, there are basically two options to profit.

- The first option PayFacs can make money is through the sale of the software that is used to provide their services. PayFacs make use of the Software-as-a-Service (SaaS) model, and their sub-merchants pay a subscription fee for using this software.

- The second option for PayFacs to profit is to charge a small fee for each of the payments they enable a merchant to make.

Overall, it should be said that payment facilitation as a service can hardly be considered as a high-margin business: PayFacs represent only one of the links in a payment processing ecosystem’s value chain. Because of this, it makes sense to start big in this business niche and allocate more resources from the outset as this will help establish a truly profitable online payment facilitation business.

Advantages of Payment Facilitation

PayFacs bring a diverse host of advantages to the table of the merchants they work with. And these advantages start from the very outset – already with…

Streamlined Onboarding

Traditional payment processing starts with opening merchant accounts with the acquirer’s bank that first needs to be identified by the merchant. Usually, the account opening process is a lengthy procedure that can take weeks and involves a stringent underwriting procedure that is especially difficult for fledgling businesses that lack business history. Payment Facilitation spares merchants the hassle of account opening, dramatically cutting the time spent on the procedure and multiplying their odds to be qualified.

Enhanced User Experience

One can say that PayFacs provide better user experiences for several reasons. Dealing with money, a customer always wants to be safeguarded against error, and the customer experiences PayFacs provide tend to be maximally error-proof. Some 80% of payment facilitators provide 24/7 support, which helps quickly solve the relatively small number of payment-processing issues that arise.

Using a PayFac’s services rids a merchant of the need to regularly transfer funds from their merchant account to their bank account – the PayFac will transfer the money that is due to them from the master merchant account to the company’s bank account, thus regularly saving the merchant both time and effort.

Lastly, it’s relatively easy for payment facilitators to team up with independent software vendors that build software solutions for those businesses that can benefit from the ability to quickly accept payments. This kind of business synergy has come to be known as embedded payments and creates improved customer experiences for small businesses like hairdressers, barber shops, veterinary clinics, and others.

Multiple Payment Methods and Optimized Invoice Payment Times

Working with a payment facilitator allows merchants to quickly encompass a diverse array of payment methods and establish a business presence on online marketplaces. Furthermore, in case of need, they can easily and conveniently impose recurrent payments and expect minimum invoice payment times as it is easy to pay invoices via a payment facilitator.

Cost-Effectiveness

With PayFacs, you pay per-transaction fees while the other payment-processing providers charge monthly fees that they can sometimes combine with per-transaction fees. Additionally, facilitation payment reduces the number of chargebacks, and, as a consequence, the related cost.

Finally, one should also mention that the vast majority of PayFacs also provide their merchants with fraud checks and payment analytics in relation to their customers and payment channels, which makes cooperation with them all the more appealing for their merchant clients.

Payment Facilitation Compliance and Legal Matters

We’ve explained why it’s worth becoming a PayFac, and have found out the strong points a facilitator potentially has to attract a client audience. Let’s now see how to start the process of becoming a PayFac – legal-wise and with regards to several other aspects.

Licensing and Registration

The process of becoming a PayFac kicks off with the candidate business looking for an authorized acquiring bank on whose behalf they will perform payment facilitation. Getting registered with an acquiring bank includes getting registered with the credit card networks. Please note that registering with the credit card networks involves paying a fee. For example, Mastercard and Visa charge $5K annually.

The candidate companies must apply to an acquiring bank, present their complete business plans and financial information, and undergo what is normally a time-consuming and effort-intensive underwriting and approval process. The bank would normally check your business processes and the technology you use with a view to assess your ability to properly underwrite merchants, prevent fraud, and handle chargebacks. Generally, businesses that already have established customer-vetting processes in place pass the procedure more easily. A payment facilitation agreement with an acquiring bank allows the PayFac-to-be to get sponsored for providing facilitation payment services.

In addition to the registration with an acquirer, it is also necessary to purchase the required licenses. The specific licenses to be obtained depend on the countries where your business is based. For example, for the UK this would be the Electronic Money Institution license.

PCI DSS, AML and KYC

As any other entity operating in the financial technology industry, a payment facilitator should be fully compliant with payment processing regulatory requirements, including but not limited to the ones of PCI DSS, PCD2, SOC2, AML and KYC. So, before you get started with establishing a payment facilitation company, make sure to research and understand the regulatory landscape in the region where you operate. For example, PCD2 is a payment data security standard applicable to businesses operating in the EU. PCI DSS, in turn, doesn’t have geographical boundaries and is a global fintech data security standard, pillared upon six main principles while each of which has its specific recommendations and requirements to meet.

Need to make sure your business is sufficiently PCI DSS-compliant?

Our PCI DSS Compliance checklist can be helpful in achieving this goal.

Implementing KYC standards and the other aspects of a full-value AML program is another major aspect of becoming a duly established PayFac. Thus, a PayFac must develop a reliable mechanism of performing the KYC procedure, as well those for risk assessment, transaction monitoring, and staff training.

Fraud Detection and Protection

To become a full-fledged PayFac, your business must implement reliable anti-fraud protection. In order to do this, PayFacs often employ advanced Machine Learning technology.

More particularly, a PayFac must have robust anti-fraud protection in place during the underwriting process with a view to detecting fraudulent merchant applications. This can include checks against various databases and black lists, geolocation checks, and 3d-party validation. Besides, it is also essential to develop functionality that allows detecting fraudulent transactions and preventing the resulting fraudulent chargebacks.

-

PCI DSS compliance implementation.

-

KYC verification procedures.

-

AML transaction monitoring.

-

Secure customer data storage.

-

Fraud prevention controls.

-

Regulatory licensing requirements.

-

Merchant risk assessment.

-

Audit and reporting procedures.

-

Data privacy compliance (GDPR, CCPA).

-

Continuous compliance monitoring.

Key Considerations Before Becoming a PayFac

Being a rather low-margin business, online payment facilitation can become a rewarding business only when a PayFac meets several important criteria.

Factor | Typical Range | Business Impact |

|---|---|---|

Initial Investment | $500K – $2M | Significant upfront capital required for infrastructure, licensing, and compliance setup |

Time to Market | 6–12 months | Longer launch timeline due to regulatory approvals and system development |

Annual Operating Costs | $200K+ | Ongoing expenses for compliance, fraud prevention, support, and infrastructure |

Break-Even Point | High transaction volume required | Profitability depends on scaling to millions of transactions |

Revenue Streams | Transaction fees, SaaS fees, value-added services | Multiple monetization options, but margins per transaction are relatively low |

Scalability Potential | High | Revenue grows with transaction volume and ecosystem expansion |

Risk Exposure | Medium–High | Includes regulatory, fraud, and operational risks that must be actively managed |

Factor

Initial Investment

Time to Market

Annual Operating Costs

Break-Even Point

Revenue Streams

Scalability Potential

Risk Exposure

Typical Range

$500K – $2M

6–12 months

$200K+

High transaction volume required

Transaction fees, SaaS fees, value-added services

High

Medium–High

Business Impact

Significant upfront capital required for infrastructure, licensing, and compliance setup

Longer launch timeline due to regulatory approvals and system development

Ongoing expenses for compliance, fraud prevention, support, and infrastructure

Profitability depends on scaling to millions of transactions

Multiple monetization options, but margins per transaction are relatively low

Revenue grows with transaction volume and ecosystem expansion

Includes regulatory, fraud, and operational risks that must be actively managed

Because of this, one should carefully consider their ability to satisfy these criteria prior to making a decision to kick off.

- Expected ROI. Assessing the odds of your payment facilitation business achieving a positive and sufficient ROI is the primary criterion you should focus on. Carefully calculate all your expenditures and take into account that a PayFac is likely to become profitable only when it starts processing several dozen million transactions.

- Costs. Businesses that want to engage in providing facilitation payment as a service must necessarily be aware of the significant costs they must be prepared to incur. The upfront costs may constitute approximately $500 000 – $2 million, while the recurring annual costs are likely to be several hundred thousand dollars too.

- Payment Infrastructure Development. When becoming a PayFac, you must be ready to invest in an array of high-quality systems to provide the key business processes no PayFac can do without.

In particular, one should be ready to bankroll the development of payment facilitation software, including advanced fraud detection software, and, in some instances, custom payment gateway development. If the latter is not the case and you decide to use an existing payment gateway, one will need to perform a secure and reliable integration with this payment gateway.

Key Takeaways

- Payment facilitation simplifies payment acceptance by allowing merchants to operate under a PayFac’s master merchant account instead of opening individual merchant accounts.

- Faster onboarding, simplified payment acceptance, integrated compliance processes, and support for multiple payment methods make the PayFac model attractive to merchants.

- PayFacs generate revenue through transaction fees, software subscriptions, value-added services, and payment-related products.

- Successful PayFac businesses depend on efficient underwriting, transaction monitoring, merchant funding, chargeback management, and fraud prevention capabilities.

- Compliance is a foundational requirement. PCI DSS, AML, KYC, PSD2, SOC 2, licensing, and card network registration obligations must be addressed before launching operations.

- Becoming a PayFac requires significant upfront investment in technology infrastructure, compliance programs, fraud prevention systems, and operational processes.

- Organizations considering this model should understand the broader technical, regulatory, and operational Fintech development challenges.

In short: payment facilitation creates meaningful value for merchants through faster onboarding, streamlined payment acceptance, and improved operational efficiency. However, building a successful PayFac business requires substantial investment, strong compliance capabilities, robust technology infrastructure, and enough transaction volume to achieve sustainable profitability.

FAQ

What does it cost to become a registered payment facilitator?

Becoming a PayFac requires a substantial upfront investment. Organizations should typically expect initial costs ranging from approximately $500,000 to $2 million, depending on the target markets, licensing requirements, technology stack, compliance scope, and operational model. These costs include payment infrastructure, registration fees, licensing, compliance programs, fraud prevention systems, underwriting capabilities, and merchant onboarding processes.

In addition to the initial investment, annual operating expenses can reach several hundred thousand dollars or more. Ongoing costs often include compliance monitoring, PCI DSS assessments, KYC and AML operations, fraud management, legal support, transaction monitoring, cloud infrastructure, and personnel responsible for risk, compliance, and operations.

The total investment varies significantly depending on transaction volume expectations, geography, regulatory requirements, and whether the organization develops proprietary payment technology or relies on third-party platforms.

What are the legal risks of operating as a PayFac without proper registration?

Operating as a payment facilitator without the necessary registrations, sponsorship agreements, licenses, or compliance controls exposes an organization to significant legal and financial risk. Regulatory authorities, acquiring banks, and card networks can impose penalties, terminate business relationships, restrict payment processing activities, or require suspension of operations.

Organizations may also face liability for inadequate KYC, AML, sanctions screening, transaction monitoring, or merchant underwriting practices. Failure to comply with PCI DSS requirements or regional financial regulations can result in fines, audits, reputational damage, and increased scrutiny from regulators and payment partners.

Because payment facilitation involves handling regulated financial activities, legal compliance should be treated as a core business function rather than an administrative requirement.

How long does it take to get approved as a payment facilitator?

The approval process varies depending on the acquiring bank, target markets, licensing requirements, and the maturity of the organization’s compliance and operational capabilities. In most cases, becoming a PayFac takes several months because acquiring banks conduct extensive due diligence on the applicant’s business model, financial stability, technology infrastructure, underwriting processes, fraud prevention controls, and compliance programs.

Organizations that already have established capabilities in merchant onboarding, KYC, AML, risk management, and transaction monitoring generally move through the approval process faster. Conversely, businesses building these capabilities from scratch often require additional preparation before being considered ready for sponsorship.

The timeline may also increase when multiple jurisdictions, additional licenses, or card network approvals are required.

What are the most common PayFac compliance failures?

Many PayFac compliance failures stem from weaknesses in merchant onboarding, transaction monitoring, and risk management. Inadequate KYC procedures, incomplete AML controls, ineffective sanctions screening, poor merchant underwriting practices, and insufficient fraud detection are among the most common issues identified during audits and reviews.

Organizations also frequently struggle to maintain PCI DSS compliance, monitor merchant activity at scale, and document compliance processes consistently. As transaction volumes increase, operational shortcuts can create significant regulatory exposure.

The most successful PayFacs treat compliance as an ongoing operational capability supported by dedicated teams, automated monitoring systems, regular audits, employee training, and continuous process improvement.

How do payment facilitators make money, and what affects profitability?

PayFacs primarily generate revenue through transaction fees charged on payments processed for merchants and through subscription fees for the software platforms that support payment acceptance. Many providers also create additional revenue streams through value-added services such as analytics, fraud prevention tools, reporting capabilities, embedded finance products, and merchant services.

Profitability is heavily influenced by transaction volume, merchant acquisition costs, chargeback rates, fraud losses, compliance expenses, infrastructure costs, and payment processor fees. Because payment facilitation is generally a relatively low-margin business, scale plays a critical role in achieving sustainable returns.

PayFac businesses typically become significantly more attractive financially when they process tens of millions of dollars in transaction volume and can spread compliance, infrastructure, and operational costs across a large merchant base.