Building a payment processing app involves creating secure infrastructure for digital transactions and integrating payment gateways and banking APIs. the key features include payment authorization, transaction tracking, recurring billing, and multi-payment method support. Modern payment apps also rely on encryption, tokenization, AI-driven fraud detection, and compliance with PCI DSS, KYC, and AML regulations to ensure secure and reliable payment experiences.

In our previous articles, we focused on how to develop a payment gateway, including a thorough description of each component, and its impact on the overall efficiency and functionality. This time, we will take a look at another participant in the process of conducting financial transactions, and provide you with our insights on how to build a payment processing app.

A 2026 market report estimates that the global payment processing/payment processing solutions market was valued at approximately $173.38 billion in 2025, and is projected to reach $208.57 billion in 2026, continuing strong double-digit growth driven by digital payments, embedded finance, and real-time payment adoption. If you are considering entering this market and looking to develop a payment processor, this article, powered by our fintech software development services experience, will guide you along the way.

How to Build a Payment Processor App

Before getting started with payment processor development, let’s briefly clarify the concept of a payment processor as such. A payment processor or payment processing app is an umbrella term used to describe solutions including but not limited to mobile payment apps, digital wallets, POS systems, P2P payment apps, Apple Pay, Google Pay, direct debit, crypto wallets, and cross-border payment solutions. All these applications have payment processing technology at their heart. A payment service provider (PSP) acts as a third-party organization that facilitates online transactions, verifies digital payments, transfers funds from buyers to merchants, and supports various payment methods to ensure transaction versatility and customer convenience.

Find out how to build a payment processing company from the ground up.

Understand the Payment Processing Essence Before You Start

At the start of the payment process, a credit card holder uses a payment gateway to enter their credit card data. Both payment processors and payment gateways are essential, distinct components within the transaction processing system: payment gateways are customer-facing, handling the secure intake of sensitive customer data and credit card details, while payment processors operate behind the scenes to authorize and settle transactions.

The payment gateway first collects and authenticates this data, ensuring the transaction is bona fide and securely handling sensitive customer data and credit card details. If the validation result is positive, the payment gateway encrypts the credit card and transactional data—referred to as payment information—and sends it to a payment processor for further processing as part of the transaction process.

The payment processor picks up the payment information and conveys it to the cardholder’s card-issuing bank, often via payment networks, for transaction authorization. The cardholder’s bank checks the transaction amount against the balance in the cardholder’s bank account with them, and either authorizes or declines the transaction.

If the validation result is positive, the payment processor relays the transactional details from the cardholder’s bank to the merchant’s acquiring bank for the latter to settle the transaction, depositing the funds into the merchant account. Corresponding push notifications about the transaction result are sent to the merchant.

Therefore, a payment gateway only provides a secure intake of the credit card and transactional data, while the payment processor handles the rest of the transaction. This explains the technical complexity of building a payment processing system. Still, we have such experience within the framework of one of our major projects.

The team from SPD Technology built a direct-to-merchant, all-in-one omnicommerce Poynt Processing payment solution in 5 months, completing tight deadlines related to the start of the business season. This solution supports processing credit card data, as well as other methods, like recurring payments. In the first 10 months following the launch of Poynt Processing, the number of active merchants exceeded 200, and relatively soon the number increased to thousands.

The solution kept rapidly gaining in popularity and started drawing a great deal of interest on the part of major market players. In February of 2021, the Poynt project was acquired by GoDaddy (NYSE: GDDY), a $14B company for $320 million.

Now, let’s proceed with discovering how to build a payment processing app step-by-step.

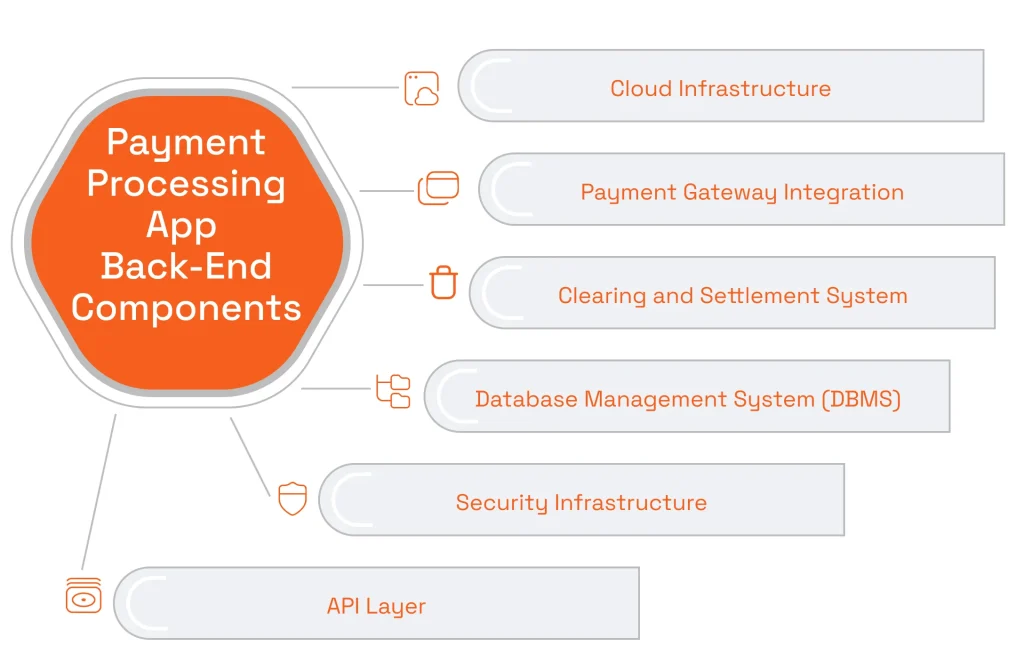

Take a Look Into Payment Processing App Back-End Components

Payment processing system architecture is complex and includes various back-end components working together to facilitate secure and efficient transactions. When building a payment processing app, it is crucial to design a scalable architecture that can support business growth and handle increasing transaction volumes. Here’s an overview of each component.

Cloud Infrastructure

This is the network of servers, storage, and computing resources that are hosted and managed by third-party providers. It allows payment processing systems to scale easily, provide high availability, and reduce infrastructure management overhead. Cloud infrastructure enables the payment system for processing to handle varying workloads, improve reliability, and enhance performance. It also allows for the seamless integration of other components and services, including support for multiple currencies, which is essential for facilitating international transactions and currency conversion.

Why is cloud infrastructure a better solution for payment processing systems compared to having servers on-premise? There are a few significant advantages of having your servers in the cloud:

- Scalability. Cloud services allow payment processing systems to scale resources up or down based on demand. This scalability is particularly important for handling varying transaction loads, especially during peak times such as holidays or promotional events.

- Cost optimization. Cloud services typically operate on a pay-as-you-go model, allowing organizations to pay for the resources they use, and ensuring cost flexibility.

- Business continuity. Your payment system will remain operational even in the event of hardware failures or other issues, since cloud providers offer geographically distributed data centers, providing high availability and redundancy.

- Data security. Ensuring data security in Fintech has always been of the utmost importance, and reputable cloud providers invest heavily in security measures, including encryption, access controls, and regular audits. They often have dedicated security teams to monitor and respond to potential threats.

According to Precedence Research, Infrastructure as a Service (IaaS) Market size was valued at $106.04 billion in 2025, with top players being Amazon Web Services, Inc., EMC Corporation, Google Inc., IBM Corporation, and Microsoft Corporation. There are enough viable options of high-end cloud providers for your solution!

Payment Gateway Integration

Your system should be able to effectively integrate with gateways. Processors and gateways often provide APIs that allow seamless communication between the two. Those APIs define a set of rules and protocols that enable different software applications to interact with each other. More specifically, APIs enable the exchange of transaction data between the merchant’s platform, the payment processor, and the payment gateway. For businesses with specialized needs, developing a bespoke payment gateway solution can offer enhanced control, security, and customization compared to standard integrations.

Need a deeper look into how to approach payment gateway integration? Find the step-by-step instructions in our detailed guide.

Additionally, some processors on the market offer Software Development Kits (SDK) that include pre-built libraries and tools to simplify the integration process. SDKs provide a set of pre-coded functions and modules that developers can use to implement payment functionality more quickly. However, custom payment gateway development and custom payment solutions can further enhance data security and provide a tailored user experience, allowing businesses to address unique requirements and improve overall efficiency.

To build custom APIs and SKDs, you need to hire a dedicated development team with a deep understanding of the Fintech industry, domain expertise, and proven experience with completed projects. Building your own payment gateway as a custom solution offers strategic advantages, such as greater control, flexibility, and the ability to adapt to evolving business needs.

Teaming up with a company that excels at payment gateway integration services will help you overcome all complexities at this phase.

Clearing and Settlement System

Clearing involves the process of matching and reconciling transactions between buyers and sellers, while settlement involves the actual transfer of funds. Payment providers and service providers play a crucial role in facilitating the transfer of money between parties during settlement, ensuring secure and seamless movement of funds. The clearing and settlement system ensures that transactions are accurately processed and funds are transferred between the relevant parties, including other financial institutions that may act as partners or endpoints in the transaction processing system. The clearing and settlement system plays a vital role in ensuring that financial transactions are settled accurately and on time.

Here are the main steps that need to be taken to develop these sub-systems:

- Clearly define the requirements of the clearing and settlement system, including the current regulations and payment processing compliance standards in the financial industry.

- Design the overall architecture and determine how the system will interact with other components such as gateways, databases, service providers, payment providers, and external financial institutions.

- Develop mechanisms to capture and store transaction data, including details such as transaction amount, timestamp, involved parties, and any relevant metadata.

- Build functionality for reconciling accounts to ensure that transactions match across different ledgers. Implement automated reconciliation processes to identify and resolve discrepancies efficiently.

- Develop processes for settling funds between different parties involved in a transaction, ensuring that payment providers and service providers can transfer money securely.

- Define settlement periods and cycles.

- Implement robust risk management solutions and fraud prevention mechanisms.

- Develop reporting features that provide insights into the clearing and settlement process.

- Implement robust security measures to protect sensitive financial data. Utilize encryption, secure APIs, and follow best practices for securing financial transactions.

- Ensure that the clearing and settlement system complies with relevant financial regulations and industry standards.

- Conduct thorough testing in a controlled environment to ensure the reliability and accuracy of the system. Perform unit testing, integration testing, and end-to-end testing.

- Plan for ongoing maintenance and updates, follow the changes in the standards and compliance. Regularly review and enhance the system to address any emerging issues, improve efficiency, and incorporate new features.

Struggle to understand payment processing compliance specifics? Our experts prepared a comprehensible guide into this matter.

Database Management System (DBMS)

The next important component on your way to build a payment processor is a Database Management System (DBMS). It is responsible for storing, organizing, and managing the data related to transactions, customer information, payment data, and other relevant details. The DBMS ensures the secure handling of sensitive payment data, providing a structured and secure way to handle data in compliance with industry standards.

The DBMS is crucial for maintaining a reliable and consistent database, ensuring data integrity, and supporting efficient retrieval of information. It helps in managing customer accounts, transaction history, and other data associated with payment processing.

Security Infrastructure

Security is paramount in the development of any Fintech project. From implementing KYC standards in Finance to robust measures such as encryption, tokenization, firewalls, and other security protocols, protecting against fraud and data breaches is critical. These security infrastructure elements are essential to safeguard sensitive data, prevent unauthorized access, and ensure compliance with industry standards.

When you develop a payment app, the most important security elements you need to get familiar with include:

-

Strong encryption protocols, including TLS and end-to-end encryption.

-

Tokenization for secure credit card data storage and transmission.

-

Strict access controls and role-based permissions.

-

Secure API architecture and authentication practices.

-

Firewalls and intrusion detection systems (IDS).

-

Regular security audits and penetration testing.

-

Multi-factor authentication (MFA) for user verification.

-

Checksums and hash functions for data integrity validation.

-

Advanced financial analytics, Machine Learning, and Artificial Intelligence for fraud detection and anomaly monitoring.

-

Incident response and disaster recovery planning.

-

Database encryption for sensitive financial data.

-

Regular software updates and patch management.

-

PCI DSS 4.0 compliance and network security controls.

-

Employee cybersecurity awareness training.

-

Physical security measures for servers and data centers.

API Layer

The API layer provides a set of interfaces that allow different components of the payment processing system to communicate and exchange data, and enable seamless integration with external services, as well as applications.

Andrii Semitkin

Delivery Director at SPD Technology

“Previously, we mentioned that APIs are required for integrating gateways, however, the API layer facilitates interoperability between other components too, allowing third-party services, mobile apps, or other systems to connect to the payment processing system.”

So, having a well-designed API layer, ensures flexibility, scalability, and the ability to adapt to changing business requirements.

Analyze Payment Processing App Features

With back-end components out of the way, let’s talk about the most important features your payment app needs to have to keep up with existing solutions. Providing a smooth payment experience is crucial for customer satisfaction and operational efficiency, and custom payment solutions can help businesses achieve this by tailoring the app to their specific needs. User experience is a vital consideration, as it directly impacts transaction success rates. Additionally, developing a payment processing app involves defining business requirements and understanding transaction volumes to ensure scalability and reliability.

MVP Features | Advanced Features | |

|---|---|---|

| User Authentication | Basic user registration and login | Multi-factor authentication, biometric authentication, and single sign-on (SSO) for enhanced security |

| Transaction Processing | Simple payment initiation and processing | Advanced transaction routing, real-time payment tracking, and support for diverse payment methods |

| Payment Gateway Integration | Integration with a basic payment gateway | Integration with multiple payment gateways, support for international transactions, and adaptive routing |

| Tokenization | Basic tokenization for card data | Advanced tokenization with token vault management for enhanced security |

| User Account Management | User profile creation and basic account settings | Enhanced account management with user roles, permissions, and customizable profiles |

| Transaction History | Basic transaction history for users | Comprehensive transaction reporting, analytics, and search capabilities |

| Notification Service | Basic transaction notifications | Configurable and real-time notifications for users, merchants, and administrators |

| Reporting and Analytics | Basic transaction reports | Advanced analytics with customizable dashboards, fraud detection, and anomaly detection |

| Customer Support Tools | Basic customer support features | Integrated customer support tools, ticketing system, and live chat for rapid issue resolution |

| Cross-Border Payments | No, or basic support for cross-border transactions | Enhanced features for managing currency conversion, cross-border fees, and compliance with international financial laws |

| Audit and Logging | Basic logging for troubleshooting | Comprehensive audit logs, user activity tracking, and compliance auditing features |

MVP Features

- User Authentication

Basic user registration and login

- Transaction Processing

Simple payment initiation and processing

- Payment Gateway Integration

Integration with a basic payment gateway

- Tokenization

Basic tokenization for card data

- User Account Management

User profile creation and basic account settings

- Transaction History

Basic transaction history for users

- Notification Service

Basic transaction notifications

- Reporting and Analytics

Basic transaction reports

- Customer Support Tools

Basic customer support features

- Cross-Border Payments

No, or basic support for cross-border transactions

- Audit and Logging

Basic logging for troubleshooting

Advanced Features

- User Authentication

Multi-factor authentication, biometric authentication, and single sign-on (SSO) for enhanced security

- Transaction Processing

Advanced transaction routing, real-time payment tracking, and support for diverse payment methods

- Payment Gateway Integration

Integration with multiple payment gateways, support for international transactions, and adaptive routing

- Tokenization

Advanced tokenization with token vault management for enhanced security

- User Account Management

Enhanced account management with user roles, permissions, and customizable profiles

- Transaction History

Comprehensive transaction reporting, analytics, and search capabilities

- Notification Service

Configurable and real-time notifications for users, merchants, and administrators

- Reporting and Analytics

Advanced analytics with customizable dashboards, fraud detection, and anomaly detection

- Customer Support Tools

Integrated customer support tools, ticketing system, and live chat for rapid issue resolution

- Cross-Border Payments

Enhanced features for managing currency conversion, cross-border fees, and compliance with international financial laws

- Audit and Logging

Comprehensive audit logs, user activity tracking, and compliance auditing features

User Authentication

At the very least, your solution needs to have basic user registration and login functionality. If we talk about more advanced features, having Multi-Factor Authentication, Single Sign-On (SSO), or even Biometric Authentication will be a great idea to ensure the highest level of security even at the stage of login.

Quality assurance and rigorous testing are critical to ensure secure and reliable user authentication in your payment processing app.

Transaction Processing

Being at the heart of your payment processing app MVP, it will be good enough to have a simple, but yet secure and effective payment initiation and processing system. Direct payment processing enables seamless and integrated transaction handling, empowering banks and acquirers to manage payments independently with greater customization, cost savings, and improved data control. It’s important to note that payment processors and payment gateways are often confused, but they serve distinct roles in the payment processing ecosystem: payment gateways securely transmit transaction data between the customer and the merchant, while payment processors handle the actual movement of funds between accounts.

If you desire more advanced functionality, consider adding:

- Advanced Transaction Routing that involves intelligent and dynamic routing of payment transactions based on various criteria. This can include factors such as cost optimization, payment method preferences, currency conversion rates, and the performance of payment processors.

- Real-Time Payment Tracking enables users to monitor the status and progress of a payment transaction in real-time, from initiation to completion.

- Support for Diverse Payment Methods that involves enabling a payment processing system to accept payments, such as credit card payments, debit cards, digital wallets, bank money transfers, and alternative payment methods.

Payment Gateway Integration

You need to implement at least basic functionality for seamless integration with multiple payment gateways. Choosing the right payment gateway solution is crucial for your business, as it impacts transaction speed, security, and the ability to scale. Having the support of international transactions from the start will be a big plus. Payment networks play a key role in facilitating transactions through payment gateways by connecting merchants, banks, and other intermediaries to ensure smooth processing of card and digital wallet payments. If you need unique and business-specific functionality, you should consider leveraging payment gateway development services.

Tokenization

Most commonly, tokenization is used for credit card processing, protecting sensitive financial data. However, tokenization can also be leveraged for other purposes, like token vault management, providing an additional layer of security.

User Account Management

For MVP, it is essential to have user profile creation functionality with basic account settings. However, for a full-fledged product, enhanced account management with user roles, permissions, and customizable profiles is an industry standard for this type of solution. Customizable profiles should allow the user account interface to be tailored to align with the company’s brand identity, ensuring a consistent and recognizable customer experience. Additionally, continuous optimization of business processes can further enhance account management and customer service, supporting scalability and improved user satisfaction.

Transaction History

In addition to implementing basic transaction history for users, it will be nice to have automated transaction reporting, customizable analytics, and advanced search capabilities.

Notification Service

Basic transaction notifications are expected in a payment processor, but you can improve on convenience by allowing users, merchants, and administrators to configure and receive real-time notifications based on their preferences.

Reporting and Analytics

Standard transaction reports provide insights into transaction volumes, success rates, and revenue including daily, weekly, and monthly summaries with pre-defined parameters. When managing costs, it is crucial to monitor licensing fees, such as authorization and address verification fees, as these can significantly impact overall expenses. The cost of building a payment processing company can also be influenced by factors like development tools, team expertise, and regulatory compliance. If we talk about the more advanced approach to reporting, allow users to create personalized dashboards by selecting and arranging Key Performance Indicators (KPIs) and metrics, as well as implement advanced analytics tools for trend analysis, forecasting, and performance tracking.

Another welcome addition to reporting and analytics functionality will be robust Fraud Detection and Anomaly Detection mechanisms. To implement them, you need a development team with solid Machine Learning and Artificial Intelligence expertise. With their help, you will be able to build real-time Fraud Detection software that can identify unusual patterns, such as unexpected transaction amounts or irregular transaction timings.

Customer Support Tools

Standard customer support features for issue resolution include support channels like forms, FAQs, email, or contacting the manager via phone. You can enhance customer support capabilities by integrating customer support tools directly into the payment processor platform, including a ticketing system for tracking and managing customer issues, as well as live chat for real-time assistance.

Cross-Border Digital Payments

While for an MVP-level solution, limited or no support for handling transactions across international borders is suitable, for a growing business it will be a good idea to be ready for cross-border payments.

Advanced capabilities for managing complex aspects of cross-border transactions include implementing tools for managing currency conversion rates dynamically and providing tools for transparent handling of cross-border transaction fees.

Audit and Logging

The purpose of logging is to capture system events for troubleshooting purposes, so there definitely should be functionality for recording essential system events, errors, and transactions, including timestamps and basic details. Comprehensive audit logs, user activity tracking, and compliance auditing can be a great addition to expand basic audit and logging functionality and provide you with more user information to improve your processor.

Consider Front-End Development Best Practices

Whether you are considering blockchain payment processor development, a small business credit card processing solution, or a digital wallet, the following best practices will come in handy to cover your Front-End part of the solution.

Create a Clear Yet Secured User Authentication Form

Important things to consider while developing a user authentication form is implementing secure password policies and offering password strength indicators. You need to set policies for password complexity, length, and expiration, including setting measures to prevent the reuse of old passwords. It will be nice to add visual cues such as color changes, progress bars, or icons to indicate password strength and provide feedback in real-time as users type their passwords.

Avoid generic error messages, especially the ones that reveal sensitive information. Instead, specify whether the username or password is incorrect and implement account lockout mechanisms after a certain number of failed attempts.

Think of Payment Initiation Form Details

Follow the idea of a clean and intuitive design for entering payment details, which includes grouping related fields together logically, such as card details and billing address, and using intuitive labels and providing tooltips for any unfamiliar terms.

Make sure to apply input masks to format card numbers, expiration dates, and other relevant fields automatically, as well as validate and format inputs as users type to prevent errors. It will be great to have validation on the client side to display immediate feedback on errors, such as wrong fields and invalid formats.

Develop a Clear Transaction Confirmation Dialog Window

It is crucial to display transaction details in an easily scannable format for the user and clearly show the payee, amount, and any associated fees. Add in a two-step confirmation process, using a modal or confirmation dialog for the first step, and display a summary with a “Confirm” button for the final confirmation step. Don’t forget to offer a concise history of recent transactions on the confirmation screen, and use responsive design to ensure a consistent experience across devices.

Enable Transaction History and Receipts

Offer the users search functionality with filters for date range and transaction type, including group transactions by date or category for easy navigation. Use pagination or infinite scrolling based on user preferences, and load older transactions seamlessly as the user scrolls.

Ensure text contrast and readability for users with visual impairments, provide alternative text for images, and use semantic HTML for screen readers.

Use Data Visualization for a User Account Dashboard

One of the most important things here is to display account balances prominently at the top of the dashboard, as well as using clear typography and styling to make the information easily readable. You should keep in mind responsive design here as well, and prioritize essential information to fit smaller screens.

The user account dashboard is a great place to implement some visualizations for greater engagement, for example, charts or graphs with interactive elements for visualizing spending patterns and account activity.

Design an Easily Navigable Help Center Interface

Make sure to have a dedicated section for FAQs with well-organized categories, which includes a search bar with autocomplete functionality. To provide an intuitive help interface, design an easily navigable help interface with a user-friendly layout and consider offering contextual help that adapts to the user’s current context within the application.

Key Takeaways

- Building a payment processing app requires much more than transaction handling. A production-grade solution depends on scalable infrastructure, payment gateway integrations, settlement systems, security controls, and compliance-ready architecture.

- Understanding the distinct roles of payment gateways, processors, acquiring banks, and card networks is essential when designing a reliable payment ecosystem.

- Cloud infrastructure provides the scalability, resilience, and operational flexibility needed to support growing transaction volumes and international expansion.

- Security must be embedded into every layer of the application through encryption, tokenization, multi-factor authentication, fraud detection, secure APIs, and PCI DSS compliance.

- Successful payment applications balance robust back-end capabilities with intuitive user experiences, including streamlined onboarding, transaction visibility, reporting, and customer support.

- Cross-border payments, real-time analytics, AI-powered fraud detection, and advanced reporting capabilities increasingly serve as competitive differentiators.

- MVP development should focus on core functionality such as transaction processing, payment gateway integration, authentication, account management, and transaction history, while advanced features can be introduced incrementally.

In short: a successful payment processing app combines secure transaction processing, scalable architecture, strong compliance controls, and seamless user experiences. Long-term success depends on balancing performance, security, and operational efficiency while building a platform that adapts to increasing transaction volumes and evolving market demands.

FAQ

How much does it cost to build a payment processing app?

The cost depends on the scope of functionality, compliance requirements, supported payment methods, integration complexity, and infrastructure needs. A relatively focused MVP with core payment processing capabilities, gateway integrations, user authentication, transaction history, and reporting functionality may require an investment of approximately $100,000–$300,000, while enterprise-grade platforms often exceed $500,000–$1 million+ when advanced fraud prevention, cross-border payments, settlement systems, analytics, and regulatory requirements are included.

Development costs are only one part of the investment. Organizations should also budget for cloud infrastructure, security testing, PCI DSS compliance efforts, third-party integrations, monitoring systems, maintenance, and operational support. The final cost is heavily influenced by transaction volume expectations, geographic coverage, and long-term scalability requirements.

What are the most common technical mistakes when building a payment app?

One of the most common mistakes is underestimating the complexity of payment architecture. Teams often focus on front-end payment flows while overlooking critical back-end requirements such as settlement processing, reconciliation, fraud prevention, transaction monitoring, scalability, and failure recovery. These omissions can create significant operational challenges as transaction volumes grow.

Another frequent issue is treating security and compliance as post-launch activities. Weak API security, inadequate encryption, poor access controls, insufficient logging, and incomplete PCI DSS preparation can introduce substantial risk. Organizations also frequently underestimate the complexity of integration when working with payment gateways, processors, banks, and third-party financial services.

How long does it take to build a payment processing app end-to-end?

Development timelines vary depending on product scope and business requirements. A focused MVP supporting a limited set of payment methods and basic transaction processing capabilities can often be delivered within 4–8 months. More sophisticated payment ecosystems that include settlement engines, advanced reporting, fraud prevention, multi-currency support, cross-border transactions, and compliance capabilities commonly require 9–18 months or longer.

The timeline is influenced not only by software development but also by security reviews, compliance preparation, infrastructure deployment, third-party integrations, quality assurance, and production readiness activities. Organizations that define requirements clearly and establish payment partnerships early typically experience smoother delivery cycles.

What security vulnerabilities should payment app developers watch for?

Payment applications are attractive targets for attackers because they process highly sensitive financial and personal information. Common vulnerabilities include insecure APIs, weak authentication mechanisms, improper token management, insufficient encryption, inadequate access controls, credential theft, session hijacking, and exposure of payment data during transmission or storage.

Developers must also address fraud-related threats, including account takeover attacks, transaction manipulation, synthetic identity fraud, and malicious automation. Strong security programs typically combine tokenization, encryption, multi-factor authentication, real-time monitoring, anomaly detection, penetration testing, secure coding practices, and continuous compliance management to reduce risk.

What payment app features do users expect that are often missed in the MVP?

Many MVPs focus primarily on transaction execution while overlooking usability features that significantly affect customer satisfaction. Users increasingly expect real-time payment status updates, detailed transaction history, searchable receipts, configurable notifications, intuitive dispute resolution processes, and responsive customer support capabilities.

As products mature, users also look for features such as biometric authentication, recurring payments, multi-currency support, spending insights, personalized dashboards, payment method management, and cross-device consistency. While these features may not be required for an initial launch, failing to plan for them early can make future product evolution more difficult and expensive.