Payment system design often begins with a simple choice: integrate a payment gateway, enable credit card payment processing, and start accepting payments. That approach works at low transaction volume, where business logic is simple and a single gateway response seems sufficient.

However, the global digital payment market report shows that digital payment transaction value continues to grow year over year, placing increasing architectural pressure on modern payment systems.

That’s why this article focuses on reliability, financial accuracy, scalability, operational confidence, and best practices in designing a payment system. It explains how payment requests move through a system, how payment transactions are tracked over time, and how responsibilities are distributed across services to support growth without losing control.

What Payment System Design Means in Real-World Products

In product discussions, the terms payment system, payment gateway, and payment app are often used interchangeably. However, they are not the same thing.

- A payment gateway handles authorization and routes transaction data to processors or banks.

- A payment app is the interface users interact with.

- The payment system sits behind both. It coordinates how payment requests enter the platform, how transactions are executed, how status is stored, and how funds are recorded and distributed.

The payment system ensures the safe transfer of funds and minimizes the risk of errors. The aim of payment system design is to ensure the system meets business objectives while maintaining robust performance and security. Achieving this requires a clear picture of all requirements, integrations, dependencies, and payment details.

The payment system determines how a payment request becomes a confirmed payment transaction, how retries are handled, how duplicate charges are prevented, and how settlement data is reconciled with internal records. It includes payment processing logic, the payment executor that communicates with external providers, and the ledger that maintains financial truth. It also governs how payout flows transfer funds to sellers’ bank accounts. Any component that affects financial correctness or transaction state is part of the payment system.

Early-stage products often blur this distinction. An MVP may depend on synchronous card flows and store transaction status directly from provider responses. That approach works at low volume. As scale increases, asynchronous payment processing becomes standard, settlement may arrive later, and retries or partial failures become routine. A single payment service provider may no longer be sufficient.

Despite these changes, the responsibilities stay consistent. The payment system must receive payment requests, execute payment transactions via one or more providers, track payment status over time, handle failures safely, and ensure funds are transferred accurately to sellers. Providers evolve. The architectural responsibilities remain. Scaling these responsibilities often requires custom software development rather than relying solely on third-party defaults.

Payment Gateway System Design as a Subsystem, Not the System

A payment gateway performs a defined role. It accepts card or account details, tokenizes sensitive data, forwards payment information to processors or banks, and returns authorization results. It processes a payment request and returns an approval, decline, or pending status. Some gateways also support fraud checks or 3D Secure. That scope is important but limited. For organizations evaluating investment, understanding how much it costs to build a payment gateway depends heavily on the scope and compliance requirements.

A gateway does not manage the full payment lifecycle. It does not track the lifecycle of a payment request from authorization through capture to settlement. It does not own the internal ledger or ensure alignment with settlement files. Financial correctness and consistency across systems remain the responsibility of the payment system. Treating the gateway as the entire solution creates gaps that surface as volume grows. Payment gateway design must align with broader payment system design principles to avoid lifecycle inconsistencies.

Learn more about payment gateway security and how to protect transaction flows properly.

Hosted payment pages and embedded flows highlight this distinction. Companies prefer hosted payment pages to avoid handling sensitive credit card data and the regulatory complexity of PCI DSS compliance. An embedded flow provides greater control over payment web pages, checkout, and data collection, often using a widget to securely capture credit card information.

In both cases, internal orchestration is still required. The payment service must create a payment order, submit it via a payment executor, and record the outcome in a ledger service.

Depending on a single gateway also reduces flexibility. Expanding regions or adding payment service providers introduces new authorization and settlement patterns. A tightly coupled architecture makes change risky.

In a well-structured payment system, the gateway is one component. The payment executor manages provider communication, the payment service controls lifecycle state, and the ledger service maintains financial truth. This separation preserves control and adaptability.

Oleksandr Boiko

Delivery Director at SPD Technology

“A gateway can authorize a card, but it cannot protect your financial model. Real resilience comes from separating execution, orchestration, and accounting. When those responsibilities are independent yet coordinated, you gain flexibility without sacrificing financial control.”

How to Design a Payment System That Survives Scale and Failure

Designing a payment system requires following systematic procedures: understanding the problem, conducting a high-level design, diving into technical details, and validating security, scalability, and reliability. Given the sensitive nature of payment data and high transaction volumes, stringent security protocols must be implemented to ensure secure payment processing and regulatory compliance.

Payment systems rarely fail due to edge cases. They break because everyday conditions are treated as exceptions. Delayed confirmations, duplicate callbacks, timeouts, partial responses from payment service providers — these are normal operating patterns. When a payment system assumes instant confirmation and perfect sequencing, inconsistencies accumulate, leading to mismatched balances, unclear payment status, and manual reconciliation. Proactively detecting inconsistencies and issues through observability and real-time monitoring is essential to maintain system integrity.

The system should detect anomalies, failures, and suspicious activity in real time, enabling prompt intervention and reducing mean time to detect critical issues.

Building for scale means accepting that payment processing is asynchronous and often involves different services, such as analytics, billing, and risk management, each independently handling parts of the payment process. Retries are inevitable. Some payment transactions will remain pending longer than expected. External systems may return incomplete or delayed data. A resilient payment system models these realities directly. It explicitly tracks state, separates execution from accounting, and treats retries and idempotency as structural capabilities.

Many architectural discussions cite Stripe system design as a benchmark for scalability. The goal is to define principles that protect financial accuracy as the payment system grows.

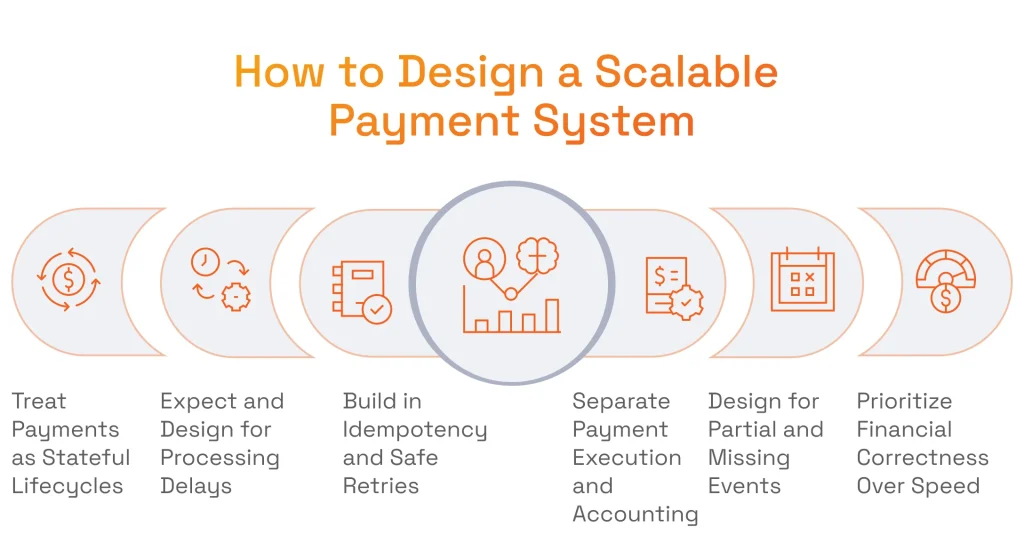

Design Payments as Stateful Processes, Not Single Requests

A payment transaction follows a defined payment cycle. Authorization, capture, settlement, and payout to a bank account may occur at different times and in different systems.

A well-structured payment system treats each payment transaction as stateful. It tracks initiated, authorized, captured, settled, failed, or pending states and records transitions between them. To manage this, the payment service typically uses two tables to track the state and details of each transaction: payment event and payment order.

When a user clicks the ‘Buy’ button, a payment event is generated, linked to a corresponding payment order, and sent to the payment service, which then stores it in the database. Each payment transaction is tracked using a unique ID stored in the payment order database table, ensuring reliable lifecycle management and preventing duplicate payments.

At any moment, the system must clearly define the current payment status. Stateless approaches rely on immediate external responses. When callbacks are delayed or retries occur, transaction state drifts. Payment events may arrive out of order. Stateful design prevents this. The payment service owns lifecycle control and applies payment service updates to reflect external changes. This structure supports scaling without losing accuracy.

Assume Payment Processing Delays Are the Default, Not the Exception

Delays are inherent in payment processing. Banks process in batches. Payment service providers apply different confirmation rules. Settlement often follows a payment request by hours or days before funds are reflected in a bank account.

As systems scale across regions, delays become routine. A resilient payment system models pending states explicitly and allows business logic to proceed safely.

System performance is often measured by the number of transactions processed per second (TPS), which is critical for understanding throughput and ensuring the system can handle high-volume or delayed payment processing efficiently.

Clear state transitions ensure the architecture does not rely on a single payment event for correctness, even when confirmations are slow.

Make Idempotency and Retries First-Class Architectural Concerns

Payment systems operate in unreliable environments. A payment executor may initiate payment service calls and receive no response while the provider processes the payment transaction. Idempotency is a system property that ensures repeated requests do not result in duplicate payments, thereby maintaining consistency and reliability.

Retries are unavoidable, especially when a payment order remains in an uncertain state. Without idempotency, repeating a payment request can create duplicate charges or inconsistent records. When a payment registration request is received, the system checks if a transaction with the same idempotency key already exists and serves the stored result if it does.

An idempotency key is a unique value generated by the client and typically has an expiration period. Idempotency keys are commonly implemented using UUIDs, as recommended by companies like Stripe and PayPal.

In this way, the payment system identifies duplicate requests and responds accordingly without processing the payment again. To prevent double payments, the system must execute a payment order at most once using idempotency checks. A unique key constraint in the database can enforce this by ensuring that only one payment request with a given idempotency key is processed.

A payment system that treats idempotency as optional is betting against reality. At scale, reality wins. Anyone attempting to build a payment processing app without an idempotent design will quickly face the risk of data duplication.

Separate Payment Flow Execution from Financial Accounting Logic

Executing a payment and recording its financial outcome are two different responsibilities. The payment executor manages external payment service calls to gateways, processors, and banks. The ledger service records debits and credits within a double-entry system.

When combined, partial failures create inconsistencies without structured payment error handling. A provider confirms a charge, but ledger writing fails. Or accounting updates before confirmation.

Clear separation avoids this fragility:

- The payment executor handles communication and retries.

- The ledger records outcomes only when state transitions are validated.

- Financial data remains consistent even if external systems behave unpredictably.

Engineer for Partial Failures and Incomplete Information

Payment processing rarely produces perfectly ordered data. Payment events may arrive late or duplicate. Settlement adjustments may revise earlier payment transaction records. Delays in compliance checks, including KYC in banking validation flows, must be explicitly modeled.

A resilient payment system expects incomplete information. It tracks intermediate states, tolerates duplicates through idempotency, and processes late events safely.

Choosing an appropriate storage solution that supports ACID transactions and delivers high performance is critical to ensure that payment events and order data are persisted reliably, even in the face of partial failures.

Designing for partial failure ensures:

- Events can arrive out of order without breaking state

- Missing confirmations trigger controlled retries

- Settlement data updates financial records safely

- Manual intervention becomes the exception, not routine work.

This approach reduces operational load over time.

Make Payment Status Communication a System Responsibility

Payment status affects users waiting for confirmation, merchants tracking revenue, support teams answering questions, and finance teams closing books. When status information is unclear, trust declines quickly.

The payment system must have status communication. That means:

- Clear definitions of states such as pending, authorized, captured, settled, and failed

- Consistent status updates across services and user interfaces

- Accurate representation of uncertainty, not premature confirmation

Executing a payment is just part of the job. Clear communication about its status reduces disputes and improves reporting. Good UI/UX design translates technical states into understandable messages.

Optimize for Financial Correctness Over Throughput

High transaction throughput can look impressive on a dashboard. Financial errors erase that impression fast. Duplicate charges, missing payouts, or incorrect balances damage credibility and may lead to regulatory scrutiny.

Oleksandr Boiko

Delivery Director at SPD Technology

“High throughput impresses stakeholders, but financial accuracy safeguards the business, especially when maintained through a double-entry system. We prioritize auditability and deterministic ledger logic. Performance tuning comes later. Incorrect balances scale faster than revenue if discipline is missing.”

Payment systems are judged by accuracy first. A slightly slower payment processing pipeline that preserves integrity is safer than a faster one that risks inconsistency.

Architectural decisions should reflect this priority:

- Strong data consistency rules for financial records

- Traceable state transitions for each payment transaction

- Audit-friendly ledgers with clear debit and credit entries

- Controlled retries that prevent duplication

As transaction volume increases, small inaccuracies multiply. Financial discipline from the beginning enables sustainable growth. Experienced fintech development companies design for auditability before optimizing for speed.

Key Challenges in Scalable Payment System Design

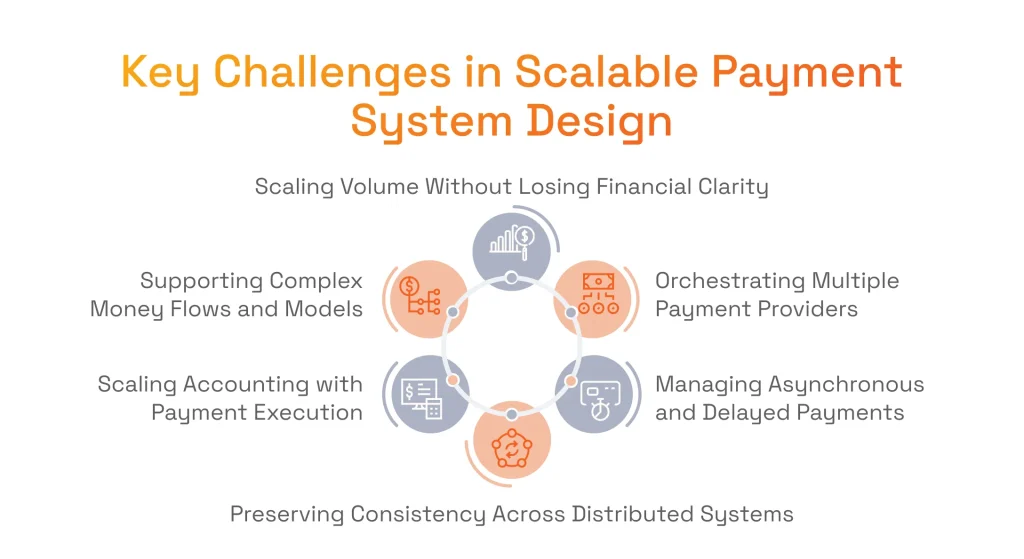

As payment systems scale, complexity increases in ways that aren’t immediately visible. Architectural limitations rarely appear as dramatic outages. Instead, they surface gradually as operational strain.

Scaling a payment system rarely fails due to an integration issue. The pressure shows up elsewhere — in reporting delays, inconsistent balances, unclear payment statuses, and growing reconciliation efforts. These symptoms indicate structural weaknesses rather than isolated technical issues.

Reconciliation becomes a critical stress point. Every night, PSPs and banks send settlement files containing the bank account balance and all transactions processed during the day. The reconciliation process compares these settlement files with ledger entries and periodically checks alignment between related services. It serves as the final line of defense for the payment system. When mismatches appear, they are classified as automated adjustments, manual corrections, or unclassifiable discrepancies. This process protects data integrity but also exposes architectural gaps.

As transaction volume grows, the number of distributed components increases as well. New regions, additional payment methods, and multiple service providers introduce divergent flows, formats, and timing rules. Assumptions that worked at a lower scale begin to break down.

The issue is rarely a failed gateway. It is a payment system design that did not anticipate scale. Teams that approach fintech software development with long-term architectural discipline reduce the risk of expensive rewrites later.

Let’s break down the most common structural challenges that emerge as payment systems grow and explain why each requires deliberate architectural decisions rather than incremental fixes.

Managing Growth in Payment Volume Without Losing Financial Clarity

Transaction growth reduces visibility. Initial efforts to integrate a payment gateway into a website rarely address reconciliation complexity at scale. Settlement files grow larger. A missing payout disappears among thousands of successful records.

At lower volume, teams often rely on provider dashboards and manual reconciliation. As requests increase, that approach fails.

A scalable system maintains clarity through:

- Structured tracking of each transaction

- Direct linkage between execution and ledger records

- Clear reconciliation with settlement files

- Reporting based on internal system data

Financial clarity does not come automatically from higher throughput. It must be preserved by disciplined state modeling and accounting logic.

Oleksandr Boiko

Delivery Director at SPD Technology

“Payment architecture needs to focus on accountability over integration. Each request needs a defined lifecycle, ledger entries linked to state changes, reconciliation rules that match settlement data, and visibility into flows. If these are unclear early, scaling worsens gaps.”

Coordinating Multiple Payment Services and Providers

Growth often forces diversification. Over time, the architecture includes several payment service providers operating side by side. McKinsey describes the rise of payment orchestration platforms as a response to provider fragmentation.

New products often introduce their own integrations. Over time, the stack expands. Integrating diverse payment methods is challenging because effective payment gateway design requires consistent abstraction layers. Each gateway exposes a different API, making provider abstraction and fallback mechanisms essential for a secure and efficient payment system. Providers have different settlement file formats, refund timing, and reporting structures. Without coordination, internal logic fragments.

The challenge is consistency. A scalable system should:

- Abstract provider-specific flows behind a unified payment executor

- Maintain consistent payment transaction states regardless of origin

- Normalize settlement data before it reaches the ledger

- Isolate provider logic from core financial accounting

The payment service defines standard lifecycle states. The payment executor translates provider-specific responses into that standard. The ledger records financial outcomes using unified rules. Providers remain interchangeable components rather than structural anchors. That discipline prevents growth from fragmenting.

Handling Asynchronous and Delayed Payment Processing at Scale

Modern payment processing systems are asynchronous by design. A credit card payment authorization may be instant, but the funds are settled later. International payments and alternative flows, including cash payment settlements, extend delays. Mobile payment gateway integration frequently amplifies asynchronous confirmation patterns.

As scale increases, pending payment requests become more common. Teams need clarity on whether a payment request is authorized, captured, or awaiting settlement.

A mature payment system defines explicit states:

- Authorized but not captured

- Captured but not settled

- Pending external confirmation

- Awaiting payout to a bank account

Clear communication of payment execution status supports business logic and financial reporting. Delay cannot always be removed. It must be made visible and predictable.

Preserving Data Consistency Across Distributed Payment Components

As payment solutions scale, they become distributed. Payment processing, accounting, fraud checks, and reporting operate independently. External payment service providers add more variables. In a distributed system, maintaining data consistency is critical as payment components operate asynchronously.

Payment events may arrive late, be duplicated, or be out of order. Settlement file updates may revise earlier assumptions and trigger additional payment service updates about transactions. Without coordination, transaction status drifts.

A disciplined payment system defines:

- Authoritative ownership of the payment state

- Strict transition rules

- Separation between operational and financial records

- Reconciliation processes to correct drift

Eventual consistency is acceptable for many features, not for financial balances. A disciplined payment system ensures convergence to correctness even when services disagree temporarily.

Scaling Financial Accounting Alongside Payment Execution

Payment execution scales with infrastructure. Accounting scales with record volume and audit requirements.

Every authorization, refund, and payout adds ledger entries. Over time, accounting volume may exceed active payment transactions. Query performance and reconciliation complexity increase.

A robust payment system must ensure:

- Atomic ledger writes

- Immutable historical records

- Clear linkage between payment execution and ledger entries

- Efficient querying without rewriting history

Execution can tolerate delay. Accounting cannot tolerate incorrect balances.

When evaluating internal infrastructure strategy, reviewing how to build a payment gateway helps clarify the separation between execution and accounting logic.

Data models must evolve carefully. New fee or payout logic should not corrupt past records. The accounting discipline must remain stable as the system grows.

Supporting More Complex Business Models and Money Flows

As products evolve, complexity increases. Industry reports on the growth of digital wallets and marketplaces note increasing accounting and payout complexity.

Marketplaces split a transaction among multiple recipients. Wallet functionality, similar to patterns seen in Venmo system design, requires internal balance tracking. A wallet service must ensure that balances accurately reflect deposits and adjustments before transferring funds to a bank account. Subscriptions add recurring revenue recognition.

Each of these models increases accounting complexity.

A single checkout may generate a payment order that produces platform fees, seller earnings, tax allocations, and deferred revenue. Funds may be held before release to a bank account.

To manage this safely, payment solutions must support:

- Separate ledger accounts for users, sellers, and platform fees

- Clear payout rules tied to verified balances

- Traceable links between original requests and downstream splits

- Configurable fee and commission logic.

Maintaining Operational Confidence as the System Evolves

A payment system affects support, finance, product, and engineering. Inconsistent data reduces trust quickly.

Support teams need clear explanations for request states. Finance relies on predictable settlement and accurate bank account reconciliation. Operational confidence depends on clarity and stability. Reliable AI for fraud detection strengthens that confidence by reducing disputed transactions.

A resilient system provides:

- Unified definitions of transaction states

- Deterministic state transitions with traceable history

- Reliable linkage between external provider data and internal records

- Controlled change management for financial logic

As new service providers and business models are introduced, historical records must remain intact. Ledger entries must stay auditable.

How SPD Technology Approaches Payment System Design

We at SPD Technology treat payment system design as a structural decision that determines long-term reliability. Our experts provide structured examples and clear explanations to clarify every aspect for our clients.

Each engagement starts with an architectural analysis of payment flows, settlement patterns, payout logic, and reporting requirements before tools or providers are selected. This structured approach also applies to mobile payment app development initiatives.

The objective is to define how the payment solution behaves under both normal and failure conditions. Payment executors manage communication with external providers. The payment service coordinates the lifecycle state. The ledger records debits, credits, and balances independently from execution responses. This model keeps financial data stable even when integrations behave unpredictably.

Vendor neutrality guides implementation. We make sure logic is not tied to a single gateway or processor. Abstraction layers normalize provider responses so additional payment service providers can be introduced without disruption. Architectural abstraction also supports stronger data security in fintech apps across multiple providers, regional expansion, and evolving product strategies.

The result is not just an integration, but a payment architecture that remains predictable as transaction volume and complexity grow.

Conclusion

A payment system is more than a mechanism for moving funds. It is a structured lifecycle that manages state, risk, accounting, and communication. Authorization temporarily locks funds on the buyer’s credit card account. Settlement, reconciliation, and payout complete the picture.

When architecture reflects that lifecycle, the system scales reliably. When it does not, status inconsistencies, ledger corrections, and reporting gaps appear. These problems typically originate in early structural assumptions.

If your payment solution is moving from a supporting role to a business-critical foundation, architectural clarity becomes essential. SPD Technology works with fintech teams and enterprises to design payment systems that remain reliable at scale and resilient to change.

Contact our experts for a focused review before structural issues grow costly.

FAQ

What is payment system design?

Payment system design defines how requests move through a platform from initiation to settlement and payout. It covers payment processing logic, status tracking, retries, ledger recording, and reconciliation. The goal is to ensure financial correctness, scalability, and clear ownership of payment state across services.

What is the difference between a payment system and a payment gateway?

A payment gateway handles authorization, tokenization, and routing data to third-party payment processors or banks. A payment system includes the gateway but also manages lifecycle state, retries, accounting logic, settlement reconciliation, and payout flows. The gateway is a component. The payment system is the structure around it.

When should a business design a custom payment system?

When transaction volume increases or complex money flows arise, a custom design is necessary. Marketplaces, wallets, subscriptions, and international payments often require architectural control beyond standard.

What is a payment gateway system?

A payment gateway system is the technical infrastructure that connects a platform to external payment processors. It manages secure data transfer and authorization responses, but does not own accounting or lifecycle control.

How to build a scalable payment system?

Start with clear state modeling, idempotent execution, separation between payment executors and ledger logic, and normalized integration with providers. Architecture decisions matter more than tools.

How is a payment system design interview different from a generic system design interview?

A generic system design interview mostly covers scalability, databases, caching, and architecture. A payment system design should include financial constraints, payment lifecycles, idempotency, reconciliation, ledger separation, and failure handling. Unlike banking system design, which centers on internal accounts, payment interviews emphasize external provider integration, asynchronous settlement, and financial accuracy.