The lending industry today is under intense pressure from rising loan volumes, evolving regulatory expectations, and persistent margin compression. Traditional manual processes simply can’t keep pace with loan processing automation, as they slow approvals, incur excess costs, and expose institutions to errors and compliance gaps.

For manual loan processing, it can take from a few days to weeks to analyze documents and borrower information. It frequently depends on manual data entry, where staff enter information into several data systems, leaving ample room for devastating errors that can damage the company’s reputation and lead to compliance issues.

Additionally, escalating operational costs, resulting from the need to hire more specialists and invest in training, can reduce profit margins as loan volumes grow. In contrast, automation secures reliable and consistent data throughout the entire process, cutting errors, streamlining decision-making, and granting comprehensive coverage from application to disbursement and risk management.

Fortunately, finance leaders already recognize that automation is a primary investment in business continuity and competitiveness. A study by McKinsey shows that financial institutions without automation capabilities waste significant resources on manual case handling and compliance reviews. Automation, however, is much more than a speed driver; it is an architectural choice aimed at organizational auditability, consistency, and adaptability along lending lifecycles.

When done correctly, automation provides a resilient backbone for steady growth and regulatory change, while poor execution amplifies operational risks and makes systems that were never meant to scale more fragile.

In this article, we will discuss how to implement a purposeful automation architecture and make your lending platform truly future-proof.

Key Takeaways

- Automated loan processing is a vital architectural decision for resilience, scalability, and competitiveness.

- An automated loan approval system must operate as a part of a broader, multi-layer architecture that combines workflow orchestration, AI/ML-driven decisioning, compliance controls, and real-time data synchronization.

- Modern platforms are designed with auditability, regulatory rule engines, and structured exception handling at their very core.

- Automation strategies should be closely aligned with the actual specifics of each lending model.

- Long-term success depends on process re-engineering, modular integration, and scalable infrastructure.

Why Loan Processing Automation Is No Longer Optional

Automation has already become a key necessity for lenders. The loan origination and loan application processes are central to the lending business, and automation streamlines these workflows through integrating multiple steps within a centralized system. Nowadays, automated loan workflows are important not only for accelerating approvals but for enforcing consistent decision logic, maintaining audit trails, and guaranteeing scalable governance across expanding portfolios.

Automating the loan lending process also leads to faster loan application processing, which is necessary for increasing customer satisfaction through quicker approvals and better client experience. Organizations which fail to modernize their lending infrastructure by ignoring progress in fintech software development risk higher costs, slower decision-making, and greater compliance exposure.

Additionally, automation can increase loan origination volume and loan approval rates by speeding up underwriting and credit issuance, and by improving the accuracy of borrower creditworthiness assessment. Automated loan processing can greatly reduce approval times from days to minutes, directly raising customer satisfaction.

Rising Origination Volumes

As financial products become easier to access and digital channels expand, loan application volumes increase exponentially. A manual underwriting approach simply fails to meet this, especially when managing substantial volumes of loan applications across multiple product types and loan amounts, leading to processing slowdowns. Automation dramatically improves process efficiency and scalability within financial services by decreasing dependence on manual tasks and enhancing workflows. Automated loan processing decreases manual data entry and document verification, cutting operational costs and improving data accuracy.

Regulatory Scrutiny

Regulatory requirements are now more stringent than ever, requiring traceability, transparency, and consistent decision logic. By using automated systems and structured workflows, audit trails can be established, improving visibility into compliance and reducing regulatory risk.

Automation supports regulatory compliance by maintaining all necessary data security standards and ensuring that industry regulations are met, with real-time checks and complete audit trails for full transparency. Automated systems also provide a detailed auditing trail, automatically logging each step of the loan process to improve compliance and build trust with customers. Additionally, automation supports maintaining data integrity throughout the loan process, verifying along with safeguarding financial data to reduce errors and fraud risks. Financial institutions continually invest in automation to strengthen governance, advance operational control, and enhance risk management capabilities.

Manual Data Entry Bottlenecks in Underwriting & Document Validation

Manual verification, credit analysis, and document review are common bottlenecks in underwriting, commonly requiring resource-intensive processing before automation can be effectively implemented. Processes built around employees, as well as fragmented systems, are both major factors in errors and inconsistencies. Automation allows for accelerated borrower data validation, information integration across systems, and workflow orchestration to reduce delays and operational risk. Automation also reduces data entry mistakes and accelerates the underwriting process, cutting application processing times from days to minutes.

Margin Erosion from Operational Inefficiency

There is a direct correlation between profitability and process efficiency, especially in an environment of rising operational costs and compressed margins. Automation helps to decrease operating expenses by lowering manual labor, rework, and human errors, while also minimizing risk-associated losses through more accurate credit reports and advanced risk assessment tools. Automating recurring tasks can decrease operational expenses by up to 50% and improve productivity by 35–50%, eliminating low-value, error-prone manual workflows. This allows teams to focus on risk assessment and customer involvement rather than administrative work.

Customer Expectation for Near-Instant Approvals

Users now expect lightning-fast experiences with transparent, close-to-instant credit decisions. Meeting these borrower expectations for speed, transparency, and speedy updates is essential in today’s mortgage industry. Automation allows real-time decision support and faster approvals while continuing control and compliance, directly responding to these demands.

Borrowers benefit from 24/7 access to digital application portals, instant document upload capabilities, and faster loan decisions. The implementation of automated loan processing leads to higher borrower satisfaction due to faster and more accurate loan decision-making, resulting in greater client loyalty and a better overall customer experience.

What “Loan Processing Automation” Really Means in 2026

While no longer synonymous with robotic process automation (RPA) or task-level scripting, true automation is a multi-layer architecture that orchestrates workflows, intelligence, compliance, and system integration inside a unified operating model. Intelligent automation and automated loan processing systems are transforming the financial services industry by improving the entire loan lifecycle, improving accuracy, ensuring regulatory compliance, and elevating human expertise.

For executives, understanding the architectural scope, as well as the true capabilities of AI/ML development, is essential to building automation that scales sustainably rather than creating isolated efficiency gains. These automated systems operate with little human involvement, providing up-to-the-minute insights into loan status and full visibility into active loans, payments, and risk trends, which improves transparency, enables smarter analytics-based decisions, and improves customer satisfaction.

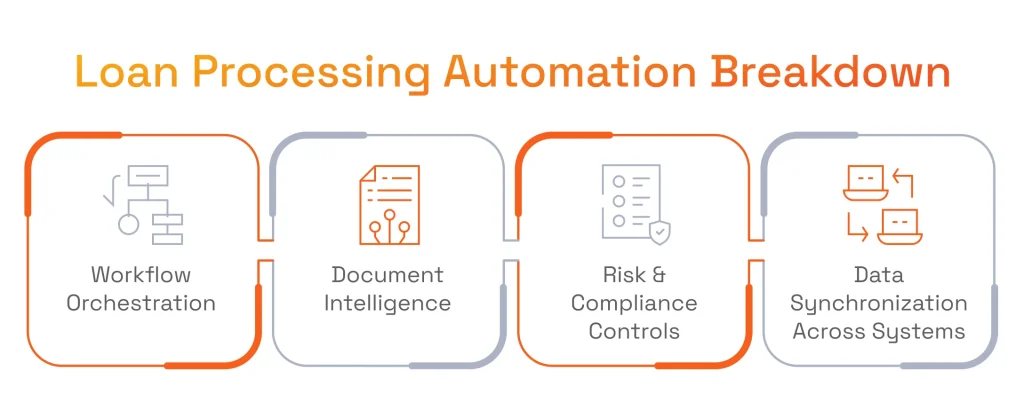

Workflow Orchestration

This is a critical element for modern platforms, as they handle the entire loan lifecycle, from application intake to decisioning. Loan origination automation improves the loan cycle from application to disbursement, ensuring regulatory compliance, preserving detailed auditing trails, and improving transparency at every stage.

Digital application intake captures structured and unstructured data across channels, with structured data being automatically organized and securely stored to improve precision and productivity. Credit scoring integrations pull bureau data and alternative data sources in real time. Underwriting cases are dynamically routed based on risk tiers, loan type, and loan amount. Decision engines trigger approvals, conditional offers, or manual reviews using configurable rules and model outputs. Automation provides better visibility into active loans, payments, and risk trends. This orchestration layer assures transparency, SLA tracking, and measurable throughput across the portfolio.

Document Intelligence

Embedded document intelligence is a big part of automation, as OCR combined with NLP extracts data from income statements, tax returns, bank statements, and identity documents with pinpoint accuracy. Intelligent document processing (IDP) plays a key role in document management by using AI and ML to read, analyze, extract, and standardize data from loan documents, simplifying document collection, verification, and storage. AI can also analyze unstructured data from documents, further improving the speed and accuracy of loan processing.

AI solutions also help to cross-check information, validate income, and alert on any errors. AI for fraud detection analyzes behavioral, transactional, and document-level signals to easily identify synthetic identities or manipulated records. So ultimately, document intelligence augments underwriting, decreasing manual review time while tightening control.

Risk and Compliance Controls

Governance built into the architecture by design is fundamental for sustainable automation, as audit trails should log the slightest data change, model inputs, and decision outcomes. With exception-handling workflows, edge cases will be escalated immediately without disrupting other processes.

Automation also secures consistent data and streamlines data collection throughout the loan origination process, supporting compliance and increasing accuracy. Regulatory rule engines allow institutions to modify quickly to meet jurisdictional requirements and internal policy changes. This layer turns automation into a risk-managed operating system that satisfies internal audit and regulatory scrutiny.

Data Synchronization Across Systems

Loan processing automation must synchronize data across the enterprise ecosystem. This integration confirms that approved loans are booked without any manual re-entry. Automated loan processing systems also integrate with accounting software to ensure reliable and consistent financial data across the organization, supporting smooth data movement and supporting accurate analysis of cash flow and income trends.

CRM synchronization maintains consistent customer records, as well as communication and payment histories. Payment processing connections allow seamless tracking of disbursements and repayments. Integrations with third-party data providers — credit bureaus, identity verification services, open banking platforms — keep underwriting inputs current and reliable.

Serhii Leleko

ML & AI Engineer at SPD Technology

“Loan processing automation is no longer viewed as a bot performing repetitive tasks. Today, it is considered an interconnected, policy-aware architecture that combines orchestration, intelligence, compliance, and integration into a scalable lending engine. Executives who approach automation at this systems level position their institutions for long-term efficiency, resilience, and competitive differentiation.”

Loan Automation Specifics in Different Lending Models

An automation system can’t be viewed as one-size-fits-all solution. Each model will face variable economic pressures, regulatory criteria, and certain operational nuances. The architecture made for traditional banks may fail in embedded finance, while the BNPL engine would struggle in sophisticated SME underwriting. Any successful automation strategy starts with aligning system design with the specifics of a lending segment.

Retail & Commercial Banks

Banking in one of those sectors that is forced to operate under massive regulatory pressure, while at the same time some players still rely on old infrastructure. Compliance obligations, like KYC in banking, audit requirements, and strict reporting standards, shape every lending decision. So, here automation should focus on structured exception handling, transparent decision logic, and traceability.

Automation further streamlines the processing of commercial loans by allowing faster application management, financial documentation, and underwriting, while supporting loan officers in evaluating applicants, checking credit history and income, and managing documentation throughout the application, processing, and closing stages.

It is critical for banks not to focus exclusively on the speed advantages of automation, but to remember that risk-first architectures that operate efficiently with all existing systems are just as important. Traditional institutions benefit most from automation when it strengthens compliance resilience plus operational control first, and accelerates processing times later.

Learn about the top banking software development companies in our featured article, where we compare the best service providers.

Digital-First Lenders / Neobanks

For lenders working exclusively in the digital realm, the main challenge is entirely different, as they handle enormous application volumes and their customers expect close-to-instant approval. Neobanks are tasked with delivering quick decisions without compromising underwriting accuracy. The goal here is to deliver event-driven and scalable automation even under the most extreme loads.

Automated underwriting has a vital role in accelerating decisions by using AI and predefined rules to assess creditworthiness and generate agreements efficiently. Automation enables loan specialists and highly skilled underwriters to deal with complex ‘exception’ cases, while routine, low-risk applications are auto-approved by the system. In addition to speed, digital lenders deal with challenges in sustaining decision quality at scale.

Embedded Finance & BNPL

For embedded finance and buy-now-pay-later models, it is another area of focus. In this scenario, decisions are made in third-party ecosystems, mostly at checkout, so latency is a big factor in partner revenue and conversion rates. That’s why, automation here should be lightweight, optimized for ultra-low responses, and API-first. Data security here is more relevant than ever, since transactions cross multiple platforms. It is safe to say that in embedded lending, automation can be considered a revenue engine connected to user experience, and not just an operational tool.

Alternative / Non-Bank Lenders

Higher credit risk and greater reliance on dispersed, non-traditional data sources are the reality for alternative lenders. In this scenario, the combination of advanced analytics and adaptive scoring models can become a true differentiator for success. Here, machine learning enhances loan decisioning and fraud detection by allowing automated systems to assess borrower risk, verify documentation, and improve decision accuracy. Machine learning algorithms can continuously learn from data to improve fraud detection proficiency in loan processing.

Automation must tightly integrate AI/ML development efforts with workflow orchestration to ensure decisions remain consistent, explainable, and scalable. For these institutions, automation becomes a strategic benefit by enabling smarter, data-driven risk modeling.

SME & B2B Lenders

This category manages complex documentation, highly nuanced financial assessments, and hybrid underwriting processes that include manual review layers. Automation here should focus on intelligent processing and structured human-in-the-loop controls. AI-driven systems can quickly verify income sustainability and process loan agreements efficiently, assuring that borrowers’ ability to preserve consistent income is assessed accurately and that loan agreement documents are interpreted, validated, and processed with speed. AI can also analyze unstructured data from documents, improving the speed and accuracy of loan processing.

Instead of substituting human expert judgement, tech solutions should boost it by lowering administrative burden, improving transparency, and organizing data. In SME lending, well-designed automation amplifies expertise while continuing disciplined oversight.

Serhii Leleko

ML & AI Engineer at SPD Technology

“I can say with confidence that in all aforementioned use cases, automation strategy should be built on operational realities and economics of the specific lending segment. Architecture-thinking is what really makes a future-proofed solution, not a set of the latest trending tools.”

Common Failure Points in Loan Automation Projects and How SPD Technology Prevents Them

Unfortunately, many loan automation projects fail to reach their full potential when foundational architectural risks are ignored. True success is built on handling systemic weaknesses and then scaling a solution.

Automating Broken Processes

The first mistake many make is to digitize already inefficient or segmented workflows. By doing this, companies simply accelerate their errors and vulnerabilities without any progress on optimization. Automating broken processes without proper re-engineering is capable of perpetuating data entry mistakes, as automation may replicate manual errors and fail to verify data validity, resulting in unreliable information during the loan approval process. Here at SPD Technology, we always start by re-engineering processes, cutting redundancies, and restructuring workflows before implementing any automation layers.

Lack of Architectural Ownership

Another unfortunate common trend is that automation projects often launch in multiple departments without unified governance. This leads to unsteady integrations and fragmented decision logic, wasting resources on automation initiatives in the first place. That’s why we form clear architectural accountability from the start, conducting analysis and aligning business strategy, risk policy, and system design into a holistic framework.

Legacy Core Banking Constraints

It is common for dated systems to pose difficulties for flexible integration and to limit live data access. By fully grasping the risks of system replacement, our team focuses on designing modular, API-driven orchestration layers that efficiently coexist with legacy infrastructure. As proven by our numerous successful use cases, this gradual modernization approach lowers disruption while increasing agility and flexibility.

Poor Exception Management Logic

Having structured exception logic in place is important for any automation initiative. Lacking this could cause severe consequences, in which the system either becomes overly rigid or operator overrides reduce traceability. Our engineers implement transparent escalation routes, highly explainable decision models, and auditable workflows to keep risk controls intact.

Compliance Blind Spots

The lack of documentation or traceability for automated decisions eventually increases regulatory exposure. SPD Technology integrates governance controls directly into the system architecture and enforces strong data security in fintech apps, ensuring compliance requirements are embedded from the very beginning.

Scaling Issues Under Peak Demand

Many automation systems perform well under normal conditions but fail during high-volume spikes. To prevent this from happening, SPD Technology applies load modeling and durable infrastructure design to guarantee uniform performance under stress.

How SPD Technology Designs Loan Processing Automation Systems

Automated loan processing systems are most effective when they are built on a well-defined methodology. SPD Technology approaches automation as an engineering discipline — combining business analysis, system architecture, and regulatory awareness into a unified delivery model. As one of the leading fintech development companies focused on scalable infrastructure, we support lenders with long-term, future-proof modernization.

Discovery & Lending Workflow Audit

We start every partnership with an extensive analysis of the existing lending processes, current integrations, and possible operational bottlenecks. Our experts map out all workflows across origination, underwriting, document validation, and decision execution to identify any inefficiencies as well as risk exposure. During this audit phase, automation streamlines data collection via efficient gathering and verifying borrower information, which improves accuracy, speeds up processing, and improves decision-making efficiency. This phase guarantees that automation addresses real business constraints and is tangible and highly effective.

Risk-First Architecture Design

Data governance and traceability are at the core of any automated loan processing system. Our risk-first architectures embed audit trails, structured decision logic, and transparent exception handling into every solution we deliver. Automation also guarantees data integrity throughout the loan processing sequence by verifying, safeguarding, and maintaining the precision of financial data at every stage. In our projects, compliance is technically enforced, and manual processes are not responsible for following it.

AI/ML Integration Strategy

As well-recognized experts in creating cutting-edge Artificial Intelligence and machine learning solutions, we know how to strategically implement this technology within workflow engines to boost fraud detection, credit scoring, and risk prediction. Machine learning additionally enhances the assessment of borrower creditworthiness by automating data validation and risk assessment, supporting more accurate and efficient underwriting decisions.

67% of finance leaders who adopted AI report high expectations about its impact, according to Gartner, and our clients are among them, experiencing the value of AI/ML implementation in their projects and achieving tangible results.

Where required, our team applies natural language processing expertise to process unstructured data, including financial documents, contracts, and customer communications. AI components are deployed in a controlled and explainable manner to preserve regulatory transparency.

Compliance Mapping

We embed regulatory alignment in the system design of our solutions from the very start. Our team maps automation logic against specific regional requirements, KYC standards, and internal risk policies of each client. This makes certain that our clients always benefit from operational consistency and audit readiness.

Incremental Modernization Roadmap

Instead of large-scale disruptive transformations, we deliver automation through phased implementation. Modular deployment reduces risk while enabling continuous improvement and system expansion.

Dedicated Engineering Team Model

SPD Technology assigns cross-functional engineers, architects, and domain specialists who serve as an extension of our clients’ internal teams. This model upholds continuity, accountability, and long-term evolution of infrastructure. Our company considers a long-term software development partnership to be our primary operational model.

Conclusion: Automation as Infrastructure, Not a Feature

Automated loan processing has become core infrastructure for modern organizations, as overall digitization in the lending market already reached $19 billion. To compete in the modern market, companies must design their processing architecture, integrate data, and operationalize risk controls across the entire lending lifecycle. Performance, compliance, as well as scalability are direct outcomes of system design.

The biggest mistake leaders can make is treating automation as an isolated project rather than a connected, essential element. When done properly and strategically, automation allows to reshape underwriting logic, strengthening governance, improving data transparency, and enabling faster decision-making without sacrificing control.

Lenders already realize that investing in architecture, not isolated improvements, is paramount. Standout companies focus on AI-driven engines, modular system design, and secure customer data management, benefiting from an unprecedented level of resilience.

If you are ready to modernize your organization’s lending infrastructure, we can design and develop an automation solution customized to your business’s particular needs. Contact us now to discuss your project!